Is Sales Commission a Period Cost? | ASC 606 & ASC 340-40

If you've ever wondered how to classify sales commissions — especially when wrestling with revenue recognition under ASC 606 — you're not alone.

Many CFOs, controllers, and revenue operations leaders ask the same question:

Is sales commission a period cost, or should it be treated differently?

In this blog, we’ll break it down clearly — no jargon, no ambiguity — so you can confidently account for commissions in line with today’s accounting standards.

Product Costs vs Period Costs: A Quick Refresher

Let’s start with the basics.

In accounting, costs are generally classified into two main buckets:

- Product Costs: These are costs directly tied to creating or delivering a product or service (like raw materials, manufacturing labor, factory overhead). They sit on the balance sheet as inventory until the product is sold, at which point they move to COGS (Cost of Goods Sold).

- Period Costs: These are costs that can’t be directly linked to production. Instead, they are expensed in the period in which they are incurred. Typical examples include rent, utilities, administrative salaries, marketing, and — you guessed it — sales commissions.

In fact, most authoritative definitions, like those from Lumen Learning, state clearly that sales commissions are considered a period cost.

Why Are Sales Commissions Classified as a Period Cost?

Here’s the simple reason: sales commissions are not a production cost.

They are incurred to drive revenue (selling the product), but not to manufacture or deliver the product itself. They’re typically tied to a sales event, not the production process.

As explained well by the Reddit accounting community here:

“Sales commissions should be an expense. They fall as a variable expense under selling costs (SG&A), typically below gross margin on the income statement.”

And that’s consistent with US GAAP guidelines.

Unless specifically reclassified under a different treatment (which we’ll cover next), sales commissions are expensed as incurred — making them a period cost.

What About ASC 606? Do Commissions Still Count as a Period Cost?

Now, here's where it gets a little more nuanced — especially for SaaS companies and those with long-term contracts.

Under ASC 606 (the modern revenue recognition standard), certain incremental costs of obtaining a contract — like sales commissions — can be capitalized and amortized over the expected benefit period of that contract.

This means that instead of expensing 100% of the commission in the current period, you spread it out over time, to match how the revenue is recognized.

In fact, our guide on how ASC 606 affects SaaS revenue recognition covers this topic in depth — especially important for subscription businesses where revenue and commissions are earned over time.

What Does ASC 340-40 Say About Sales Commissions?

When it comes to sales commissions and ASC 606, there’s an important companion standard that often gets overlooked: ASC 340-40.

ASC 340-40 (Other Assets and Deferred Costs — Contracts with Customers) provides specific guidance on how to account for the costs of obtaining a contract — such as sales commissions.

It says that if costs are incremental to obtaining a contract (meaning they wouldn’t have been incurred if the contract wasn’t signed), and if the entity expects to recover those costs, then they must be capitalized and amortized over the period of benefit.

In plain English:

✅ If the commission is tied to winning a deal, and

✅ The customer is likely to stay and generate revenue,

👉 you should capitalize the commission instead of expensing it all upfront.

The Logic Behind Both Treatments (Period Cost vs Capitalization)

1️⃣ Treating Sales Commissions as a Period Cost (Expense as Incurred)

When this applies:

- Commission is not tied to a specific contract

- Commission is for short-term or transactional activity (e.g. SDR commission for setting meetings)

- Commission is not incremental (you would have paid it anyway)

Logic:

This approach matches cost to the period it was incurred — clean, simple, and aligned with traditional GAAP. If the revenue stream is short-term, or commissions aren’t clearly linked to a long-term contract, it makes sense to expense commissions as incurred.

Implications:

✅ Simpler accounting

✅ No deferred expense on the balance sheet

🚫 Potential EBITDA volatility if large commissions are paid upfront

2️⃣ Capitalizing and Amortizing Commissions Under ASC 606 & ASC 340-40

When this applies:

- Commission is directly tied to obtaining a contract

- The contract has a multi-period revenue stream

- The company expects to recover the cost over time

Logic:

By capitalizing commissions, you match the expense to the revenue period — a core principle of ASC 606. This provides a more accurate picture of profitability and aligns with how revenue is recognized.

Implications:

✅ Smooths EBITDA and earnings

✅ Aligns expenses with revenue recognition

✅ Required for audit compliance if conditions are met

🚫 Adds some complexity to accounting (which is why automation tools like Visdum are helpful)

Why This Distinction Matters for SaaS Businesses

For SaaS companies, where subscription revenue is earned over time, capitalizing commissions under ASC 606 + ASC 340-40 makes a lot of sense — and in many cases, is required.

Meanwhile, some companies may choose (or be required) to treat certain short-term commissions — such as SDR spiffs — as period costs. And that’s okay too — the key is consistency and compliance.

For real-world examples and sample reports, check out our Practical Guide to ASC 606 Sales Commissions.

So... Is Sales Commission a Period Cost or Not?

The short answer is: It depends on how you apply ASC 606.

Choosing the Right Tools for Compliance

Handling amortization manually is cumbersome — especially as your sales team scales and contracts grow in complexity.

That’s why many SaaS finance teams are turning to purpose-built tools. Our Ultimate Guide to ASC 606 Compliance Tools walks through how leading companies automate commission expense management — ensuring accuracy, audit readiness, and peace of mind.

Final Word: Context Matters

Here’s the best way to think about it:

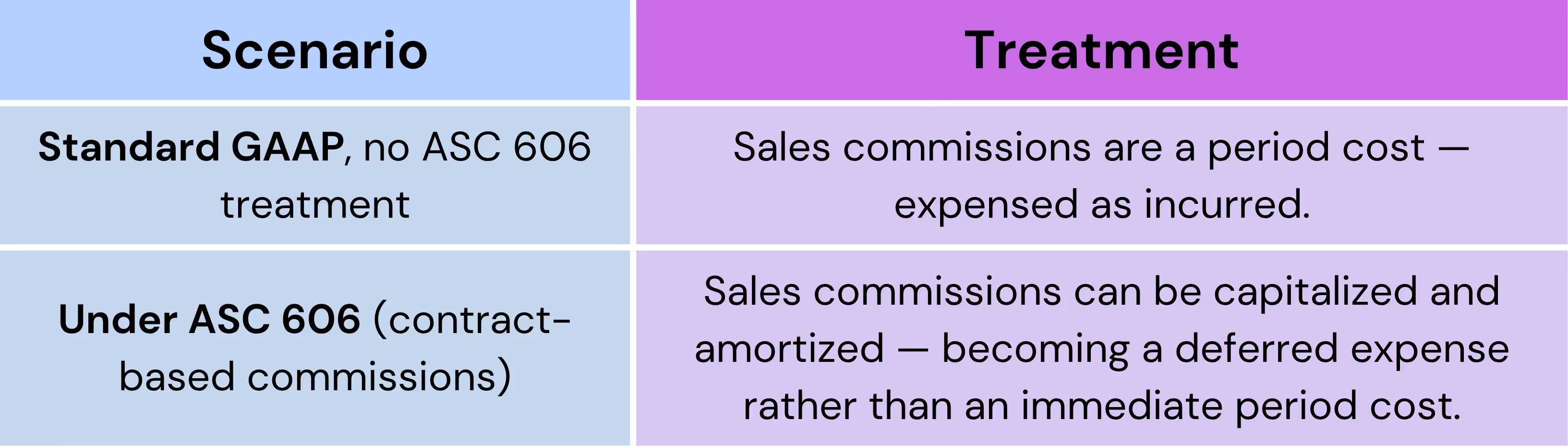

👉 If you’re not applying ASC 606 (or the commission isn’t incremental to the contract), commissions are a period cost.

👉 If you are applying ASC 606 and the commission meets the criteria for capitalization, it becomes a deferred cost, amortized over time.

It’s not about right or wrong — it’s about aligning your accounting treatment to the current standards and your business model.

Next Steps: If managing ASC 606 compliance and commission amortization is causing friction in your finance workflows, tools like Visdum’s ASC 606-compliant sales commission software can help streamline the entire process — and keep your auditors happy.

.avif)

.avif)

.webp)