The Essential Guide to ASC 606 Revenue Recognition in 2026

TL;DR

SaaS revenue recognition under ASC 606 requires recognizing subscription revenue ratably over the service period using a five-step model: identify the contract, identify performance obligations, determine the transaction price, allocate the price to obligations, and recognize revenue as obligations are satisfied. The hardest parts for SaaS are multi-element arrangements, variable consideration on usage-based pricing, and contract modifications.

SaaS revenue used to be straightforward. Customer signs, you bill, finance books the revenue. ASC 606 broke that model in 2018 and rewired it around the transfer of control: revenue is recognized when the customer receives the benefit of the service, not when they pay for it.

For SaaS companies, this changed almost everything. Subscription revenue is now recognized ratably. Setup fees usually amortize. Implementation services may or may not be distinct. Usage-based fees are variable consideration that requires estimation and constraint at every reporting date. Multi-element bundles need Standalone Selling Price documentation that holds up under audit.

Eight years in, the issues that surfaced in early adoption are still showing up in audit findings. Performance obligations get over-combined to simplify accounting or over-separated to manage timing. Variable consideration estimates lack supporting documentation. Contract modifications get processed inconsistently across deals. The pattern in 2026 is the same as in 2019: companies that treat revenue policy as a document fail audits, companies that treat it as a system pass them.

This guide covers how ASC 606 applies to SaaS revenue, the five-step model adapted for subscription contracts, and where the policy lines actually get drawn. For the broader framework, see the ASC 606 pillar guide.

Key Takeaways

- ASC 606 changed SaaS revenue recognition from upfront recognition at signing or billing to ratable recognition over the service period. A $120,000 annual contract produces $10,000 of revenue per month.

- The five-step model applies to every SaaS contract, but three steps cause the most policy debate: identifying distinct performance obligations, estimating variable consideration, and allocating the transaction price across bundled obligations.

- Multi-element contracts (software plus implementation plus support) require each distinct obligation to be priced at Standalone Selling Price (SSP) and recognized on its own pattern.

- Usage-based and consumption pricing create variable consideration that must be estimated at contract inception, constrained, and updated each reporting period.

- Setup fees that do not transfer a distinct service amortize over the contract term, not at signing. Most SaaS setup fees fail the distinctness test.

- Contract modifications (adds, upgrades, extensions) require analysis per modification: separate contract, termination and new contract, or continuation. Each produces a different waterfall.

What is ASC 606 revenue recognition?

ASC 606 revenue recognition is the FASB standard requiring companies to recognize revenue from customer contracts based on the transfer of control of goods or services, using a five-step model.

Issued jointly by FASB and IASB in 2014, ASC 606 replaced ASC 605 and unified more than 200 industry-specific revenue rules into a single principles-based framework.

For SaaS, the practical change is that revenue is recognized as the customer receives the benefit of the service, which is almost always ratable over the subscription term. The cash, the invoice, and the booking can all happen at different times, but the recognized revenue follows control transfer, not any of those events.

How does ASC 606 apply to SaaS specifically?

SaaS contracts have three characteristics that make ASC 606 application more complex than a one-time product sale:

- Subscription-based recurring revenue that delivers benefit continuously over time, not at a single transfer event.

- Multi-element arrangements that bundle software access, implementation, training, support, and sometimes hardware into one contract.

- Contract evolution through frequent modifications: seat adds, tier upgrades, term extensions, product expansions.

The five-step model handles all three, but the answers depend on how each SaaS contract is structured. Two companies with similar revenue profiles can produce very different revenue waterfalls based on how they identify performance obligations, allocate price, and treat modifications.

The 5-step revenue recognition model for SaaS

The five-step model is the operating procedure for recognizing SaaS revenue under ASC 606. Same steps as any industry, but the SaaS application has distinct interpretive choices at each one.

Step 1: Identify the SaaS contract

A contract exists when both parties have approved it, rights and payment terms are identifiable, the contract has commercial substance, and collection is probable. For SaaS, the signed order form referencing the Master Services Agreement is the contract. Pilots without firm commitment, free trials, and verbal extensions typically do not qualify until the criteria are met.

Step 2: Identify SaaS performance obligations

A performance obligation is a promise to transfer a distinct good or service. For SaaS, software access and ongoing customer support are usually distinct. Implementation may or may not be distinct: if it is required for the software to function, it combines with the software as a single obligation. If a third party could provide it, it is distinct.

Where teams trip up: over-combining bundles to simplify accounting (which distorts ratable revenue), or over-separating obligations to manage timing (which exposes inconsistent treatment across similar deals).

Step 3: Determine the SaaS transaction price

The transaction price is the amount the company expects to be entitled to. For SaaS, this includes the fixed subscription fee plus an estimate of any variable consideration: usage overages, volume discounts, performance bonuses, SLAs, and renewal incentives. Variable consideration must be estimated using either the expected value method or the most likely amount method, then constrained to amounts unlikely to be reversed.

Did you know?

The "constraint" on variable consideration is not optional. Auditors review historical accuracy of variable consideration estimates each reporting period. If estimates have been materially wrong over time, the constraint must tighten. This is one of the top audit focus areas for SaaS companies with usage-based pricing in 2026.

Step 4: Allocate using Standalone Selling Price

When a contract has multiple performance obligations, the transaction price is allocated based on each obligation’s Standalone Selling Price (SSP). For SaaS, this is rarely a directly observable number, since the company sells most things as bundles. ASC 606 allows three estimation approaches: adjusted market assessment (what would customers pay), expected cost plus margin, and the residual approach (only when the price varies significantly).

Most SaaS teams use a documented blend of the first two. The methodology must be applied consistently across deals, refreshed periodically, and supported by enough data that an auditor can replicate the calculation.

Step 5: Recognize SaaS revenue over time

Revenue is recognized as control transfers. For SaaS subscription access, the customer simultaneously receives and consumes the benefit, so recognition is "over time" on a ratable basis. A 12-month $120,000 contract recognizes $10,000 each month.

Point-in-time recognition applies in narrow cases: perpetual software licenses (transferred at delivery), one-time training sessions (recognized when delivered), and shipped hardware (recognized when control transfers).

TL;DR

The five-step model is consistent across industries, but SaaS application hinges on three judgment calls: which obligations are distinct, how to estimate and constrain variable consideration, and how to set Standalone Selling Prices for items rarely sold separately. These three are where audit findings cluster.

How do you handle multi-element SaaS arrangements?

Multi-element arrangements are the default for B2B SaaS. A typical enterprise contract bundles software access, implementation, training, and support, often with hardware or professional services layered on. Under ASC 606, each distinct obligation gets its own SSP and its own recognition pattern.

A worked example.

A $200,000 SaaS contract includes:

- Software platform access for 12 months (SSP: $150,000)

- Implementation services (SSP: $30,000, distinct because a third party could perform them)

- Customer support (SSP: $20,000, distinct)

Total SSP equals $200,000, so the full transaction price allocates directly: software at $150K (recognized ratably at $12.5K per month), implementation at $30K (recognized as services are delivered), support at $20K (recognized ratably at ~$1.67K per month).

If the same deal sold for $180,000 instead (a $20,000 bundle discount), the discount typically allocates proportionally across obligations unless evidence shows it relates to a specific deliverable. Documenting that allocation logic is the audit-defensible move.

How do you recognize revenue on usage-based and consumption pricing?

Usage-based revenue is variable consideration. The amount the customer will actually pay depends on consumption that has not happened yet at contract inception. ASC 606 requires the company to estimate this consumption, include the estimate in the transaction price, and constrain the estimate to amounts unlikely to be reversed.

Three practical implications for SaaS companies running consumption pricing in 2026:

- Estimate at inception. The transaction price at contract start must include an estimate of variable consideration, even though actual consumption is unknown.

- Constrain the estimate. Only the portion of the estimate the company is highly confident will not be reversed is recognized. Aggressive estimates create audit exceptions.

- Update each reporting period. Estimates must be revised as actual consumption data accumulates. Cumulative catch-up adjustments are recognized in the period of change.

Most teams underestimate the documentation burden here. Auditors expect a defined methodology, supporting consumption history, and consistent application across customers and contract types.

How do you treat setup fees and onboarding under ASC 606?

Setup fees in SaaS contracts are one of the most common policy errors. Most teams default to recognizing them upfront. ASC 606 usually does not allow that.

The test is whether the setup activity transfers a distinct good or service. If the setup is required for the customer to use the software (configuration, data migration, account provisioning) and produces no standalone benefit, it does not transfer a distinct service. In that case, the setup fee is treated as an advance payment for the subscription and amortized over the contract term.

A $10,000 setup fee on a 12-month contract is recognized at roughly $833 per month, not $10,000 in month one. Most SaaS setup fees fail the distinctness test and get amortized.

Setup fees that fund a genuinely distinct service (custom development, separately marketable training, configurable implementation that survives subscription cancellation) can be recognized when delivered. The key is documentation: a clear policy stating which fees are distinct and which are not, applied consistently.

How are SaaS contract modifications handled?

SaaS contracts get modified constantly: adding users, upgrading tiers, extending terms, adding modules, swapping products. ASC 606 requires each modification to be classified into one of three treatments:

| Modification type | When it applies | Revenue treatment |

|---|---|---|

| Separate contract | Adds distinct goods/services priced at SSP | Account for as a new, separate contract |

| Termination + new contract | Remaining goods/services are distinct from the original | End original contract, create new contract with combined remaining + added price |

| Continuation of existing contract | Remaining goods/services are not distinct from original | Cumulative catch-up adjustment to revenue |

Treatment depends on contract specifics: pricing relative to SSP, the nature of what is being added or changed, and whether the existing obligations are still distinct after modification. Teams that process modifications without classification analysis end up with revenue waterfalls that do not reconcile.

Modifications also have commission implications, since the related contract acquisition costs may need re-amortization or adjustment. For commission treatment, see ASC 606 Commission Amortization: The CFO Guide to ASC 340-40.

TL;DR

The hardest parts of SaaS revenue recognition under ASC 606 are not in the five-step model itself. They are in the documentation: which obligations are distinct, what the Standalone Selling Price is, how variable consideration is estimated and constrained, and how each modification gets classified. Documentation is what passes audits.

FAQ: Common SaaS revenue recognition questions

How does ASC 606 affect SaaS revenue recognition?

SaaS subscription revenue is recognized ratably over the service period as the customer receives the benefit. A $120,000 annual contract produces $10,000 per month of recognized revenue, regardless of when the customer pays.

What is Standalone Selling Price (SSP)?

SSP is the price at which an entity would sell a good or service separately. When directly observable, SSP is used. When not, ASC 606 allows estimation using adjusted market assessment, expected cost plus margin, or residual approach. Most SaaS teams use a documented blend.

How are setup fees recognized under ASC 606?

Setup fees that do not transfer a distinct service are treated as advance payments and amortized over the contract term. Setup fees that fund a separately distinct service may be recognized upfront. Most SaaS setup fees fall into the amortized category.

How is usage-based revenue recognized?

Usage-based fees are variable consideration. They must be estimated at contract inception, constrained to amounts unlikely to be reversed, and updated each reporting period with cumulative catch-up adjustments.

What is a multi-element arrangement?

A contract that bundles two or more distinct goods or services. Under ASC 606, each distinct obligation is priced at its Standalone Selling Price and recognized on its own pattern, even when the bundle is sold at a discount to the sum of SSPs.

How are SaaS contract modifications treated?

Modifications are classified as a separate contract, a termination plus new contract, or a continuation of the existing contract. Each treatment produces a different revenue waterfall. The classification depends on whether added goods are distinct and whether they are priced at SSP.

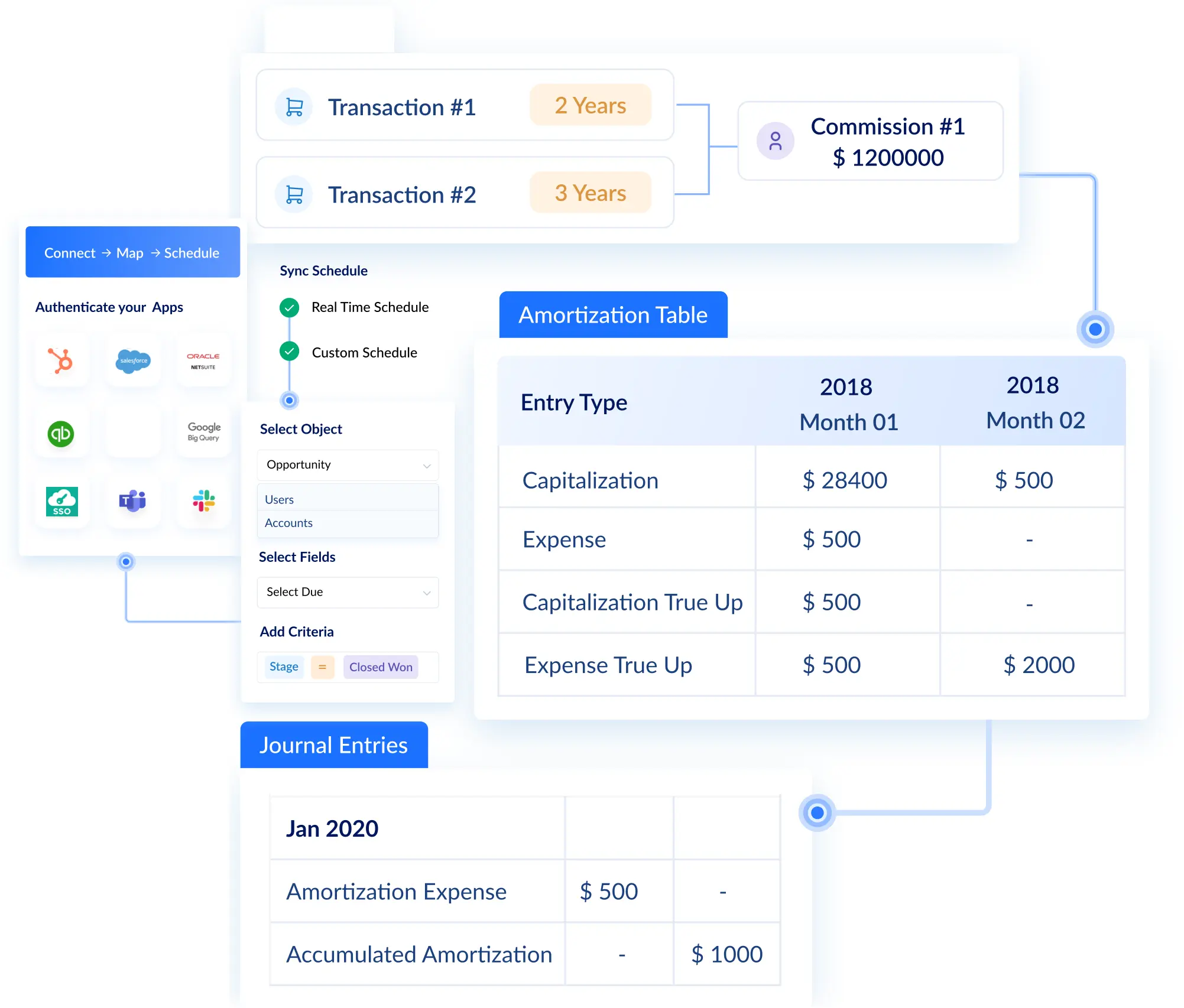

About Visdum

Sales compensation breaks at scale because it is run as a document, not a system. Visdum is the system.

Visdum is the sales compensation platform for Finance and RevOps leaders at mid-market and enterprise B2B SaaS companies. It replaces spreadsheets and legacy commission tools with infrastructure built for ASC 606 and ASC 340-40 compliance from day one: automated amortization schedules, contract-linked commission tracking, clawback handling, and audit-ready reporting that maps to your revenue waterfall.

Model amortization scenarios with the free ASC 606 Amortization Calculator, or download the SaaS CFO Advanced Revenue Recognition Reporting ebook for deeper coverage of waterfall and disclosure reporting.

To see how Visdum would work for your team, book a personalized demo or explore the platform tour.

.webp)